Algo trading programming doesn't have to be overwhelming, even for beginners. With the right guidance, you can learn to create and implement your own algorithms.

First, let's start with the basics. To begin with, you need to choose a programming language. Python is a popular choice for algo trading programming, thanks to its simplicity and extensive libraries.

You'll also need to decide on a strategy, such as trend following or mean reversion. This will help you determine the parameters and indicators to include in your algorithm.

Having a solid understanding of data structures and algorithms will also be essential. This will enable you to efficiently manage and process large datasets.

Related reading: Does Algo Trading Work

Getting Started

Getting started with algo trading programming can be overwhelming, but breaking it down into manageable steps makes it a lot simpler.

The first step is to import necessary libraries, such as pandas and numpy, which are essential for data analysis and manipulation.

These libraries are used to import data and perform calculations, making them a great starting point for your project.

Importing these libraries at the beginning of your code sets the foundation for your algo trading project.

You might enjoy: Algo Trading What Is

Strategy Design

When designing an algorithmic trading strategy, the type of algorithm employed will have a significant impact on the system's design. This will involve considering the markets being traded, the frequency and volume of the strategy, and the trade-off between ease of development and performance optimization.

A low-frequency US equities strategy will require different technology choices than a high-frequency statistical arbitrage strategy trading on the futures market. Prior to choosing a language, data vendors must be evaluated based on their relevance to the strategy at hand.

The frequency of the strategy is a key driver of the technology stack, with strategies employing data more frequently than minutely or secondly bars requiring significant consideration for performance. For high-frequency strategies, software such as HDF5 or kdb+ is commonly used for storing and evaluating extensive volumes of data.

Here are some key considerations for strategy design:

Strategy Idea

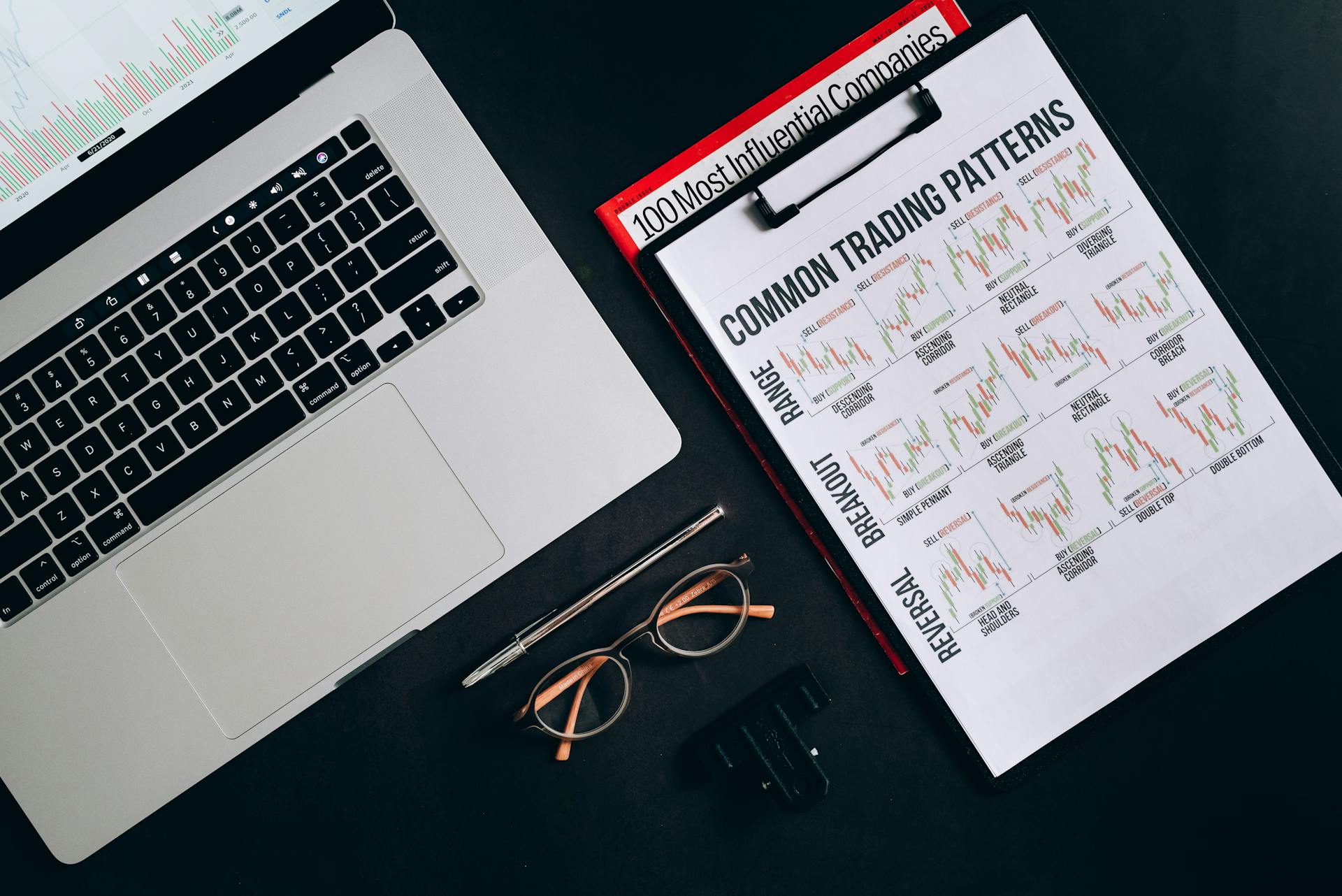

A good strategy idea should be based on a clear understanding of market trends and technical indicators.

The Two Simple Moving Average crossover strategy is a popular idea that aims to trade with the trend using a confirmation from the signal of two simple moving average indicators.

A Simple Moving Average (SMA) is a lagging technical indicator that calculates the average closing price of a specific period.

The SMA signal comes after the signal of price action, making it a lagging indicator.

This strategy uses two SMAs with different periods to generate buy and sell signals.

Here's a summary of the strategy:

- The strategy uses two SMAs with different periods.

- The SMA signal comes after the signal of price action.

By understanding how to implement a strategy like this, you'll be able to create your own trading ideas and test them in a simulated environment.

Variables and Types

Variables and Types are crucial components in strategy design. A variable is a memory location with a name associated with it, used to hold data.

In MQL5, a program can contain tens and hundreds of variables. Each variable has its scope, which determines its availability in the program.

Local variables are declared within a function and have a scope limited to the function body. Global variables, on the other hand, are declared beyond all functions and have a scope that spans the entire program.

There are several types of variables in MQL5, including:

Understanding the different types of variables and their scopes is essential for effective strategy design. By choosing the right data type for each variable, you can ensure that your strategy runs smoothly and efficiently.

If Statement

The IF statement is a fundamental tool in strategy design, allowing you to make choices based on specific conditions.

It's used when a choice must be made, and its syntax is straightforward: If the expression is true, one set of actions is taken, and if it's false, another set is executed.

The IF statement is perfect for determining the next step in your strategy, as seen in the example where the Bid value is first received, then checked against a threshold of 1.146600.

If the Bid value is above the threshold, an alert is triggered with a specific message; otherwise, a different message is displayed.

The IF statement's power lies in its ability to create conditional logic, allowing you to respond to different scenarios in a tailored way.

In the example, the IF statement is used to alert the user with a specific message based on the Bid value, demonstrating how this tool can be applied in real-world scenarios.

Statistical Arbitrage

Statistical arbitrage is a type of strategy that involves making trading decisions based on deviations from statistically significant relationships between assets. This approach is based on the mean reversion hypothesis, which expects assets to revert to their expected value over time.

Statistical arbitrage can be applied in all asset classes and can be fully automated from both analysis and execution perspectives. A wide range of statistical arbitrage strategies have been developed, including pair trading, where a ratio or spread between two stocks' prices is analyzed.

Pair trading involves buying the stock that has gone down and selling the stock that has outperformed, in the expectation that the spread will go back to its normal level. This strategy can work with a hundred or more stocks in its portfolio, which are classified according to a number of factors.

The TABB Group estimates that annual aggregate profits of low latency arbitrage strategies currently exceed US$21 billion. This is a significant amount, and it highlights the potential of statistical arbitrage as a profitable strategy.

Arbitrage is possible when one of three conditions is met: the same asset does not trade at the same price on all markets, two assets with identical cash flows do not trade at the same price, or an asset with a known price in the future does not today trade at its future price discounted at the risk-free interest rate.

Here are the three conditions for arbitrage:

- The same asset does not trade at the same price on all markets.

- Two assets with identical cash flows do not trade at the same price.

- An asset with a known price in the future does not today trade at its future price discounted at the risk-free interest rate.

These conditions highlight the importance of analyzing market prices and identifying opportunities for arbitrage. By understanding these conditions, traders can develop effective statistical arbitrage strategies that can generate significant profits.

Open Source vs Proprietary

When choosing a software for your strategy design, you have two main options: open source and proprietary.

Open source software is free to use and modify, allowing developers to collaborate and improve the code.

Proprietary software, on the other hand, is owned and controlled by a single company, which can lead to higher costs and limited flexibility.

One example of open source software is the popular project management tool, Trello, which was acquired by Atlassian in 2022.

Trello's open source nature allowed it to grow rapidly and become a widely used tool in the industry.

In contrast, proprietary software like Microsoft Project can be expensive and may require additional licenses for each user.

According to a 2020 study, 71% of businesses prefer open source software due to its flexibility and cost-effectiveness.

However, proprietary software may offer better customer support and security features, especially for large enterprises.

Ultimately, the choice between open source and proprietary software depends on your specific needs and priorities.

vs R

Python and R are both widely used in the financial analytics industry, but they have different strengths and purposes. R is traditionally favored by researchers for its statistical analysis and data visualization capabilities.

Python offers better performance in large-scale applications, making it ideal for high-frequency trading and real-time execution. This is a key advantage over R, which is more suited for smaller-scale data analysis.

R's statistical analysis and data visualization capabilities make it a great tool for researchers, but Python's versatility and integration with broader programming applications make it a better choice for developing complex trading algorithms.

If this caught your attention, see: Algorithmic Stock Trading and Equity Investing with Python

Strategy Implementation

Strategy implementation is a crucial step in algo trading programming. Most strategies are implemented using modern programming languages, such as C/C++ for high-frequency trading.

For less complex strategies, languages like Python can be used, as seen in the moving average crossover strategy example. This strategy uses a popular choice for beginners, where buy and sell signals are generated based on the crossover of short-term and long-term moving averages.

A fresh viewpoint: Strategies for Trading Stocks

The choice of language depends on the type of strategy, frequency, and volume of data, as well as the trade-off between ease of development and performance optimization. For example, a low-frequency US equities strategy will have vastly different technology choices compared to a high-frequency statistical arbitrage strategy trading on the futures market.

Opening Orders

Opening orders is a crucial step in strategy implementation, and it starts with writing code to open an order.

To write your code to open an order, you can follow the example presented earlier, which provides a clear guide on how to do it.

Opening an order requires a specific set of steps, and by following this guide, you can ensure that your code is accurate and effective.

This approach has been found to be helpful in real-world applications, where a well-written code can make all the difference in strategy implementation.

Basic Strategy Implementation

A basic trading strategy can be implemented using a moving average crossover strategy, where buy and sell signals are generated based on the crossover of short-term and long-term moving averages.

Broaden your view: Short Term Options Trading

This strategy involves calculating a short-term and long-term moving average of the closing price, with the short-term MA being 20 days and the long-term MA being 50 days.

To generate trading signals, we compare the short-term MA to the long-term MA, and buy when the short-term MA is greater than the long-term MA, and sell when the short-term MA is less than the long-term MA.

A buy signal is generated when the short-term moving average crosses above the long-term moving average, indicating an upward trend, while a sell signal is triggered when the short-term moving average falls below the long-term moving average.

We can also use a linear regression model as a basic model for strategy implementation, although more complex models such as Markov chain Monte Carlo can also be used.

Backtesting the Strategy

Backtesting the Strategy is a crucial step in evaluating the effectiveness of your trading strategy. It involves simulating trades on historical data to see how your strategy would have performed in the past.

You can use libraries like backtrader or zipline to run backtests, which provide built-in functionalities to help you evaluate your strategy.

To start backtesting, you need to define your trading strategy, which can be done using a class like MovingAverageStrategy. This class defines the rules for buying and selling based on moving averages.

Backtesting allows you to evaluate your strategy on historical data before deploying it live, giving you a clear picture of its performance.

You can also use backtesting to optimize your strategy by making adjustments based on the results. This iterative process helps you maximize returns while minimizing risks.

To visualize the performance of your strategy, you can use matplotlib to plot the portfolio value over time, as shown in the code snippet: data['Portfolio Value'].plot(title='Backtesting Result: Portfolio Value Over Time', figsize=(12, 6)).

By backtesting your strategy, you can refine it and make it more effective, ultimately leading to better trading results.

A fresh viewpoint: Universal Portfolio Algorithm

Order Modification

Order modification is a crucial aspect of strategy implementation, allowing you to adjust orders to suit changing market conditions.

In this context, the OrderModify method is used to modify the characteristics of previously opened or pending orders. This can be a powerful tool for traders, enabling them to adapt their strategies as needed.

By using OrderModify, you can adjust orders to reflect new information or changing market dynamics, helping to maximize returns and minimize losses.

Recommended read: How to Trade in Equity Market

Errors Handling Technique

Errors can and do happen in any program, so it's essential to include an errors handling technique in our code to prevent crashes and warn of any potential issues.

This technique checks every executed order or code and alerts us if something goes wrong, effectively acting as a protection mechanism for the trader and their funds.

Crashes can occur at any moment, and it's crucial to have a safeguard in place to prevent losses due to inappropriate situations.

High-Frequency

High-frequency trading is a form of algorithmic trading that involves high turnover and high order-to-trade ratios. It's characterized by highly sophisticated algorithms, specialized order types, co-location, very short-term investment horizons, and high cancellation rates for orders.

High-frequency trading firms represent 2% of the approximately 20,000 firms operating in the U.S. today, but account for 73% of all equity trading volume. This shows the significant impact these firms have on the market.

In the U.S., high-frequency trading firms are market makers and provide liquidity to the market, which has lowered volatility and helped narrow bid–offer spreads, making trading and investing cheaper for other market participants. This is a key benefit of high-frequency trading.

High-frequency funds started to become especially popular in 2007 and 2008, with total assets under management for hedge funds with HFT strategies reaching US$141 billion in 2009. However, this number decreased by about 21% from its high.

There are four key categories of HFT strategies: market-making based on order flow, market-making based on tick data information, event arbitrage, and statistical arbitrage. All portfolio-allocation decisions are made by computerized quantitative models.

On a similar theme: Currency Trading Strategy

The success of computerized strategies is largely driven by their ability to simultaneously process volumes of information, something ordinary human traders cannot do. This ability to process large amounts of data quickly is crucial for high-frequency trading.

For high-frequency strategies, a substantial amount of market data needs to be stored and evaluated, requiring significant consideration for performance. Software such as HDF5 or kdb+ is commonly used for these roles.

For more insights, see: Quantitative Hedge Fund Strategies

Risk Management

Risk management is a crucial component of algorithmic trading programming, as it helps mitigate potential losses and preserve capital. Proper risk management can make even the best strategies profitable.

Position sizing is a key aspect of risk management, and it's essential to ensure that no trade takes up more than 2% of your total capital. This is known as the "2% rule." max_risk = 0.02 defines the maximum risk per trade.

To further minimize losses, stop-loss orders can be implemented to automatically exit a position when the asset's price falls below a certain level. For example, a stop-loss order can be set at 5% below the entry price.

Additional reading: What Is Position in Trading

A trailing stop-loss order can also be used to adjust the stop-loss level as the stock price moves in your favor, allowing you to lock in profits and protect yourself from reversals. This can be achieved by adjusting the stop-loss price based on the current price and a specified trailing percentage, such as 5%.

Diversification is another effective risk management strategy, as it helps spread risk by trading a variety of assets. This can mitigate the impact of a single losing trade on your entire portfolio.

Managing Risk with Stop-Loss Orders

Managing Risk with Stop-Loss Orders is crucial to avoid substantial losses, even with the best strategies.

A good rule of thumb is to make sure no trade takes up more than 1% to 2% of your capital in a single transaction, known as the "1% or 2% rule."

You can set a stop-loss order at 5% below the entry price, for example, by using the formula stop_loss_price = entry_price * (1 – 0.05).

On a similar theme: Trade Wash Rule

A trailing stop-loss order adjusts the stop-loss level as the stock price moves in your favor, allowing you to lock in profits and protect yourself from reversals.

To implement a 5% trailing stop, you can use the function trailing_stop(current_price, trail_percentage) with trail_percentage = 0.05.

By diversifying your trades across a variety of assets, you can mitigate the impact of a single losing trade on your entire portfolio.

Here are some key takeaways for managing risk with stop-loss orders:

- Position Sizing: Limit each trade to 1% to 2% of your total capital.

- Stop-Loss Orders: Set stop-loss orders at 5% below the entry price or use a trailing stop-loss order.

- Trailing Stop-Loss: Adjust the stop-loss level as the stock price moves in your favor.

- Diversification: Spread your risk across multiple assets.

Data Quality Issues and Handling

Data quality issues can be a major roadblock in risk management, especially in algorithmic trading. Missing data points are common in financial data, particularly with lower liquidity assets or extended trading hours.

To handle missing data points, you can use interpolation techniques or fill missing data points using the fillna() method in pandas. This can be done using the following code: data = data.fillna(method= ‘ffill’) or data = data.fillna(method= ‘bfill’). These methods ensure that gaps in your dataset are filled using the previous or next available value.

Outliers and anomalies can also skew your trading strategy, causing abrupt increases or decreases in data brought on by inaccurate reports. Statistical methods like the Z-score can be used to detect and filter out these anomalies.

Here's an example of how to calculate the Z-score and filter out outliers: data['Z_score'] = (data['Close'] – data['Close'].mean()) / data['Close'].std(). By keeping only data points within three standard deviations of the mean, you can remove outliers using the following code: data = data[data['Z_score'].abs() < 3].

Spoofing

Spoofing is a strategy used by some traders to temporarily manipulate the market by giving the impression of wanting to buy or sell shares without actually intending to do so.

This is done by placing limit orders outside the current bid or ask price to change the reported price to other market participants.

The trader can then place trades based on the artificial change in price and cancel the limit orders before they are executed.

For example, a trader might place a buy order at $20.10 when the current bid is $20 and the ask is $20.20, making it seem like the best bid price is $20.10.

A market maker, thinking the best bid price is $20.10, will fill a sale order at that price, allowing the trader to sell shares for a $.10 higher price per share.

The trader can then cancel their limit order on the purchase they never had the intention of completing.

See what others are reading: What Is the Best Program for Sublimation?

Quote Stuffing

Quote stuffing is a tactic employed by malicious traders to gain an advantage over slower market participants.

These traders quickly enter and withdraw large quantities of orders, flooding the market and causing market data feeds to delay price quotes. Ordinary investors rely on these feeds, but high-frequency traders can profit from proprietary, higher-capacity feeds and the most capable, lowest latency infrastructure.

HFT firms benefit from quote stuffing, which artificially induces latencies and arbitrage opportunities. Researchers have shown that high-frequency traders can profit from these induced latencies and arbitrage opportunities.

Quote stuffing causes market data feeds to delay price quotes, giving HFT firms an unfair advantage. This tactic exploits the differences in infrastructure and feeds between ordinary investors and high-frequency traders.

Effects

Algorithmic trading has introduced a new level of complexity to markets, making them more uncertain despite individual traders' efforts to simplify communication.

The use of local rules in trading algorithms can make certain parts of the communication dynamic more predictable, but on the macro-level, the overall emergent process becomes more complex and less predictable.

This phenomenon is not unique to the stock market and has also been detected with editing bots on Wikipedia.

The development of algorithmic trading has reduced trade sizes further, even though decimalization initially caused a decrease in trade sizes.

Jobs once done by human traders are being switched to computers, with the speeds of computer connections becoming increasingly important.

In the US, spending on computers and software in the financial industry increased to $26.4 billion in 2005, highlighting the growing importance of technology in finance.

A cultural divide has emerged between employees of firms primarily engaged in algorithmic trading and traditional investment managers, with the former focusing more on data and less on sell-side research.

If this caught your attention, see: Algorithmic Trading Program

Concerns

One of the biggest concerns with algorithmic trading is its black box-ness, making it difficult for traders to understand why certain data or relationships are being used.

This lack of transparency can lead to a loss of trust between investors and companies, as warned by UK Treasury minister Lord Myners.

System failures can result in business interruption, as highlighted by the Financial Services Authority in its annual report.

A notable example of this is the 2012 technology issue at Knight Capital Group, which caused a loss of $440 million due to erroneous orders sent into the market.

High-frequency trading can also contribute to market volatility, as seen during the 2010 Flash Crash, where the Dow Jones Industrial Average plummeted 600 points only to recover within minutes.

This is a risk that needs to be carefully managed, especially in ultra-high frequency trading systems where performance is prioritized over maintainability.

Here are some of the key concerns with algorithmic trading:

These concerns highlight the importance of proper risk management in algorithmic trading, including the need for clear and transparent systems, regular maintenance, and careful monitoring of market conditions.

Market Analysis

Market Analysis is a crucial aspect of algo trading, as it allows you to analyze market trends and make informed decisions quickly.

Algorithmic trading uses automation to make decisions instantly, in contrast to traditional trading which depends on human judgment and can be slow and error-prone.

Python algorithmic trading enables you to create models that automatically manage complex portfolios and execute trades quickly without human intervention.

Suggestion: Algorithmic Trading and High Frequency Trading

Fetching Market Data

You can use APIs like Alpaca's, Yahoo Finance's yfinance, or Robinhood's robin_stocks to fetch market data for your trading bot.

Fetching historical market data is a crucial step in creating a trading strategy, and you can do this using libraries like yfinance or Alpaca's API. For example, yfinance allows you to download historical price data for a specific stock, like Apple Inc. (AAPL), over a specified time period.

To fetch historical price data using yfinance, you define the stock ticker and time period, and then use the download function to retrieve the data. This can be done in a few lines of code, making it a straightforward process.

Using Alpaca's API, you can also fetch historical data, but the syntax is slightly different. Instead of using the download function, you use the get_barset function to retrieve the data.

Regardless of the API you choose, fetching historical market data is an essential step in creating a trading strategy, and it's a great way to get started with algorithmic trading.

Market Timing

Market timing strategies are designed to generate alpha and can be developed using a methodology that includes backtesting, forward testing, and live testing.

These strategies often use technical indicators such as moving averages to make decisions.

Backtesting is typically the first stage of development, where the algorithm is simulated through an in-sample data period to see how it would have performed in the past.

Optimization is performed during backtesting to determine the most optimal inputs. Steps taken to reduce the chance of over-optimization include modifying the inputs +/- 10%, shmooing the inputs in large steps, running Monte Carlo simulations, and ensuring slippage and commission is accounted for.

Forward testing is the next stage, where the algorithm is run through an out-of-sample data set to ensure it performs within backtested expectations.

Live testing is the final stage, where the developer compares actual live trades with both the backtested and forward-tested models, using metrics such as percent profitable, profit factor, maximum drawdown, and average gain per trade.

Algorithmic trading allows for quick execution of trades, which can be beneficial for market timing strategies.

Market Making

Market making is a strategy that helps increase liquidity in the markets by facilitating a large volume of trade orders for buying and selling.

A market maker, usually a large institution, buys and sells securities of a particular set of firms, displaying buy and sell quotations for a specific number of securities.

Automated Trading Desk, which was bought by Citigroup in July 2007, has been an active market maker, accounting for about 6% of total volume on both NASDAQ and the New York Stock Exchange.

Market makers function by displaying buy and sell quotations and completing orders from their own inventory, ensuring liquidity in the financial markets.

This makes it simpler for investors and traders to buy and sell, as market makers are extremely important for sufficing trade.

Advanced Topics

In algo trading, understanding the nuances of market data is crucial, and one key concept is the use of historical data to inform trading decisions. Historical data can be used to identify trends and patterns that can inform trading strategies.

Market data is often collected and stored in large datasets, which can be overwhelming to navigate. A common approach to dealing with this is to use data aggregation techniques, such as grouping data by time period or asset class.

The choice of programming language for algo trading is also important, and languages like Python and R are popular choices due to their ease of use and extensive libraries. These libraries can simplify tasks such as data analysis and visualization.

In addition to programming languages, algo traders must also consider the importance of risk management, which can be achieved through techniques such as position sizing and stop-loss orders.

Intriguing read: Algo Trading Broker

Strategy Optimization

Backtesting is a crucial step in algorithmic trading, allowing you to evaluate your strategy on historical data before deploying it live. This process enables you to refine and optimize your strategy to maximize returns while minimizing risks.

Libraries like backtrader or zipline provide built-in functionalities to run backtests, making it easier to iterate and improve your strategy. You can use these libraries to create and test different scenarios, such as changing the parameters of a moving average strategy.

The iterative process of backtesting and optimization is key to creating sophisticated trading models. By visualizing the performance of your strategy and making adjustments based on the results, you can continuously improve its effectiveness.

Algorithmic trading strategies can be implemented using modern programming languages, and some strategies are even designed in spreadsheets. However, more complex strategies often rely on advanced techniques like linear regression, game-theoretic models, and pattern recognition.

In the financial landscape, the emergence of electronic communication networks (ECNs) and decimalization have increased market liquidity, making it easier for institutional traders to execute orders at better average prices. This has led to the development of more sophisticated algorithmic trading strategies.

The use of algorithms in financial markets has grown substantially since the mid-1990s, with foreign exchange markets experiencing a significant increase in daily turnover, reaching US$6.6 trillion in 2019. This increased liquidity has enabled the implementation of more complex trading strategies, such as those based on Markov chain Monte Carlo models.

Choosing a Language

Considerable detail has now been provided on the various factors that arise when developing a custom high-performance algorithmic trading system. The next stage is to discuss how programming languages are generally categorized.

Python is preferred for algorithmic trading, but other languages can also be used. Each programming language brings its own set of strengths and weaknesses to the table.

When deciding on a language, consider the quality of the API, language-wrapper availability, execution frequency, and anticipated slippage. The quality of the API is crucial, with well-documented APIs providing better performance and ease of access.

For more insights, see: High Frequency Trading Programming

Easy Syntax

Python's simplicity is what makes it accessible to traders who aren't seasoned developers. Its clean and intuitive syntax lets you implement complex strategies with fewer lines of code.

Python's concise syntax allows traders to quickly develop and iterate on strategies. This makes it an excellent choice for research and development in algorithmic trading.

According to Example 4, Python's simplicity is what makes it accessible to traders who aren't seasoned developers. Its clean and intuitive syntax lets you implement complex strategies with fewer lines of code.

In contrast to Java, Python's concise syntax makes it easier to prototype and test trading strategies. As mentioned in Example 5, Java's verbose syntax makes it cumbersome for prototyping and testing trading strategies.

Here are some benefits of Python's easy syntax:

- Reduces the chances of errors

- Makes it easier to understand and maintain codebases

- Cuts down on onboarding time when collaborating with a team or transitioning projects

As mentioned in Example 4, Python's simplicity makes it easier to understand which is helpful when you're collaborating with a team or transitioning projects, as it cuts down on the onboarding time.

Choosing a Language

Choosing a Language is a crucial step in developing a custom high-performance algorithmic trading system. Considerable detail has now been provided on the various factors that arise during this process.

Python is a popular choice among traders due to its simplicity and clean syntax. Its easy-to-understand codebase makes it accessible to traders who aren't seasoned developers.

Python's syntax is so intuitive that it lets you implement complex strategies with fewer lines of code, reducing the chances of errors and making it easier to maintain your codebase in the future.

The world of trading is competitive and time-sensitive, demanding quick iterations. Python's easy syntax and readability translate into faster testing and deployment of strategies, making it a highly productive tool for algorithmic trading.

Each programming language brings its own set of strengths and weaknesses to the table, so it's essential to consider the specific needs of your trading system when choosing a language.

Type Systems

Choosing a language for your trading stack requires careful consideration of its type system. A statically-typed language performs type-checking during compilation, catching many bugs that would lead to numerical errors.

Languages like C++ and Java are statically-typed, which can be beneficial for a highly numerical system like an algorithmic trading engine. However, type-checking doesn't catch everything, and exception handling is necessary to handle unexpected operations.

Statically-typed languages also allow the compiler to make optimisations that are unavailable to dynamically-typed languages. This is because the type and memory requirements are known at compile-time, resulting in improved performance.

For example, libraries like NumPy/SciPy can alleviate the performance hit of dynamically-typed languages by enforcing a type within arrays.

Here's a comparison of statically-typed and dynamically-typed languages:

Ultimately, the choice between a statically-typed and dynamically-typed language depends on your specific needs and priorities.

Frequently Asked Questions

Is Python or C++ better for algo trading?

For algo trading, Python is often preferred due to its faster development time, allowing you to get to market sooner. While C++ may offer faster execution speeds, the initial development time can be a significant trade-off.

Is algo trading really profitable?

Algorithmic trading can be profitable, offering a systematic approach to trading that can help traders execute trades more efficiently than humans. However, success in algo trading requires careful strategy and execution

How do I code for algo trading?

To code for algo trading, start by creating a trading algorithm platform and defining its approach, timeframe, and frequency of trade. Then, evaluate and refine your algorithm using historical data before connecting it to a demo trading account for testing.

Featured Images: pexels.com