Invoice payment terms and conditions are a crucial part of any business transaction, setting out the rules and expectations for when and how payments are made.

Clear and concise language is essential in payment terms and conditions, as it helps prevent misunderstandings and ensures both parties are on the same page.

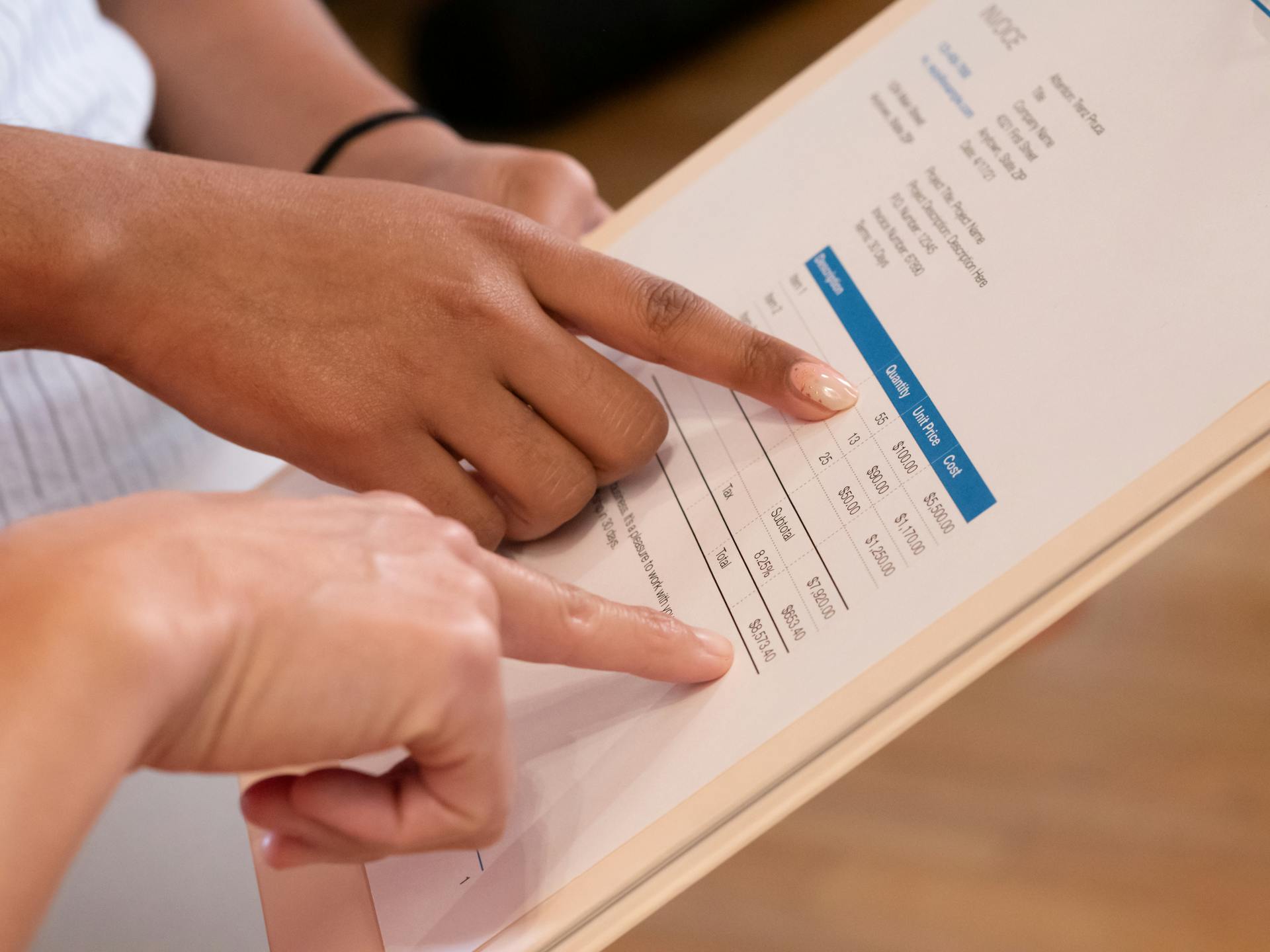

Payment terms typically include the payment method, due date, and late payment penalties, as seen in a sample invoice payment terms and conditions letter.

Understanding Invoice Payment Terms

In the B2B sector, it's essential to have clear invoice payment terms to avoid misunderstandings and ensure expectations are met. You need to consider aspects of your collaboration and stipulate in legal language to protect both parties.

Payment times and late payments are crucial to specify, as it outlines the expected payment amount and timeframe. This helps prevent disputes and ensures you receive payment on time.

You should also specify the currencies and payment forms you accept, especially if you do business internationally. This helps prevent conversion rate issues and ensures you receive payment in the agreed-upon currency.

Invoice delivery terms can also cause issues if not clearly stated. Some companies may only accept physical invoices up to a specific month's date, so it's essential to clarify these expectations ahead of time.

Here are some key payment terms to consider:

Types of Payment Terms

Payment terms can be a crucial part of protecting your business's finances. A standard payment plan is a straightforward agreement detailing the amount due and the due date.

To ensure timely payments, you can also consider an instalment plan, which specifies a series of payments over time, often including interest or finance charges. This can be beneficial for larger transactions or purchases.

Alternatively, a deferred payment plan allows for a delay in payment until a specified date, sometimes used in educational or large purchase contexts. This can provide customers with flexibility, while also giving you time to manage your cash flow.

Here are some common types of payment terms:

- Standard payment plan: A straightforward agreement detailing the amount due and the due date.

- Instalment plan: Specifies a series of payments over time, often including interest or finance charges.

- Deferred payment plan: Allows for a delay in payment until a specified date, sometimes used in educational or large purchase contexts.

50% Upfront

Asking for a 50% upfront payment can seem daunting, but it provides a significant benefit by allowing you to cover associated costs without spending out of your pocket.

Receiving a portion of the total price ahead of time can help you stay afloat during long-term projects. This can be especially helpful when working with clients who may not be able to pay in full at the start of a project.

Asking for 50% upfront also allows clients to break up more expensive payments into smaller, more manageable parts. This can be a huge relief for clients who are worried about making a large payment all at once.

It can be an excellent middle ground to take should your customers feel uncomfortable paying upfront for your services in full. This approach shows that you're willing to work with them to find a solution that works for everyone.

Net Terms: 30/60

Net Terms: 30/60 can be a bit confusing, but it's actually quite straightforward. It means that your clients have up to 30 or 60 days after receiving an invoice to finalize payments. This is often used in various industries, including B2C and B2B.

If you're wondering whether to use Net 30 or Net 60, consider the following. Net 30 is frequently used across all sectors, while Net 60 is often found in the fashion and construction industries.

You can swap out "Net 30" and "Net 60" for "30 days" and "60 days" on your invoices to prevent any confusion and potential late payments. However, it's still a good idea to include a specific due date as well.

Here's a quick rundown of what these terms mean:

Remember to include a specific due date on your invoices to avoid any confusion or potential late payments.

Offer Discounts and Late Fees

Offering discounts can be a great way to incentivize customers to pay their invoices quickly. You can offer a 1% discount if clients make the full payment within 7 days of the receipt date, or a 2% discount if they pay the next day.

It's essential to highlight your discount system on your invoice terms and conditions to make it stand out. You can do this by using bold or color to draw attention to it.

Rewarding customers with discounts for paying quickly can be more effective than charging late fees. A common example is the term "5% net 10", which provides a 5% discount for paying within ten calendar days.

Late fees can be a percentage of the invoice total, typically around 1.5%. However, regulations on late fees and interest vary from state to state, so be sure to check what's legal where you are.

If invoices remain unpaid after several attempts to collect, you may need to take more drastic steps, such as hiring an attorney or collection agency, or filing a claim in small claims court.

Creating an Invoice Payment Terms Template

Creating an invoice payment terms template is a crucial step in ensuring smooth transactions with your clients. A well-crafted template should clearly identify the parties involved.

To start, you'll want to outline the payment terms, including the amount owed, payment schedule, and method of payment. This could include bank transfers, checks, or other payment methods. The payment schedule should detail the due dates for payments, the amount of each installment, and the total amount to be paid over time.

In addition to payment terms, your template should specify whether interest will be charged on the amount owed, including the interest rate and how it will be calculated. This information can help prevent disputes down the line.

Here are the essential elements to include in your invoice payment terms template:

- Parties involved: The lender (creditor) and borrower (debtor)

- Payment terms: Amount owed, payment schedule, method of payment, due dates, and total amount to be paid

- Interest rate (if applicable): Interest rate and calculation method

- Consequences of non-payment: Late fees, additional interest, or legal action

- Termination clause: Conditions for terminating the contract

- Signatures: Both parties must sign the contract

- Governing law: Jurisdiction's laws that govern the agreement

How to Create a Discount Policy

Creating a discount policy can be a great way to incentivize customers to pay you faster. Offer a 1% discount if clients make the full payment within 7 days of the receipt date, or a 2% discount if they pay the next day.

Highlight your discount system in bold or color on your invoice terms and conditions to make it stand out. This will help customers take notice and make payment arrangements accordingly.

A 5% discount for paying within ten calendar days is a common practice, often more effective than late fees. This approach is known as the "5% net 10" term.

Late fees can be a percentage of the invoice total, such as 1.5%. However, regulations on late fees and interest vary from state to state, so be sure to check local laws.

If invoices remain unpaid after several attempts to collect, you may need to take more drastic steps, such as hiring an attorney or collection agency.

How to Create a Template

Creating a template for your invoice payment terms is a crucial step in ensuring that your customers understand what they owe and when they need to pay. To start, you'll need to identify the parties involved, including the lender or creditor and the borrower or debtor.

The contract should clearly outline the amount of money owed, the payment schedule, and the method of payment. This includes details like due dates for payments, the amount of each installment, and the total amount to be paid over time.

You'll also need to specify whether interest will be charged on the amount owed, including the interest rate and how it will be calculated. This is especially important if you're lending a large sum of money.

If the borrower fails to make payments on time, the contract should outline the consequences, such as late fees, additional interest, or legal action. This will help prevent disputes and ensure that both parties are on the same page.

A well-crafted payment agreement template should also include a termination clause, which describes the conditions under which the contract can be terminated. This could include full repayment or breach of the agreement.

To make the contract legally enforceable, both parties must sign the contract. This is a crucial step that shouldn't be skipped. The signatures will make the contract binding and ensure that both parties are committed to the terms.

Here are the essential elements to include in your payment agreement template:

- Parties involved: Clearly identify the lender or creditor and the borrower or debtor.

- Payment terms: Outline the amount of money owed, payment schedule, and method of payment.

- Interest rate: Specify whether interest will be charged and how it will be calculated.

- Consequences of non-payment: Outline the consequences of late payments.

- Termination clause: Describe the conditions under which the contract can be terminated.

- Signatures: Both parties must sign the contract to make it legally enforceable.

- Governing law: Specify which jurisdiction's laws will govern the agreement.

Managing Post-Signature

Managing post-signature can be a daunting task, especially when it comes to tracking payments and deadlines. Regularly monitor the payment schedule and contract deadlines to ensure compliance with the terms agreed.

Manually tracking payments can lead to missed deadlines, lost documents, and disputes over payment status. This can prove costly for your business. Automated contract reminders can reduce these risks and improve visibility into contracts.

Automated reminders can be sent to both parties about upcoming payments or important contract milestones, ensuring that the payment schedule is adhered to without manual follow-up. Store all signed agreements in a centralized repository, making it easy to access and review payment agreements at any time.

Here are some key features to look for in a contract management system:

- Automated contract reminders

- Centralized repository for all agreements

- Integrations with invoicing systems

These features can help you stay on top of payments and deadlines, and reduce the risk of disputes and lost documents.

Signing the Agreement

Signing the agreement is a crucial step in making a payment agreement legally binding. Both parties need to sign the contract, which can be done using wet ink signatures or electronic signatures.

The signing process can be delayed by the need for physical signatures or the inconvenience of switching between platforms for eSignatures. This slows down the entire process.

Juro solves this problem by allowing native eSigning within the same platform. This means both parties can sign the payment agreement electronically, making the execution process quick and hassle-free.

Juro's native eSignature functionality eliminates the need for printing, scanning, or physically mailing documents. Instead, parties can sign on mobile or any other device.

Juro's eSignatures are legally binding and compliant with global eSignature laws, providing peace of mind that the agreement is enforceable once signed.

Here are the benefits of using Juro's native eSigning:

- Quick and hassle-free execution process

- Eliminates the need for physical signatures or switching between platforms

- Legally binding and compliant with global eSignature laws

Managing Post-Signature

Managing post-signature can be a daunting task, especially when dealing with multiple contracts and payments. Both parties must adhere to the terms set forth in the agreement, with the borrower making payments as scheduled and the lender providing necessary documentation.

Regularly monitoring the payment schedule and contract deadlines is crucial to ensure compliance with the terms agreed. This helps prevent missed deadlines, lost documents, and disputes over payment status.

Manually tracking payments and keeping physical or fragmented digital records can lead to costly mistakes. A centralized repository for all agreements can make it easy to access and review payment agreements at any time, track payment status, and maintain a comprehensive record of all transactions.

Automated contract reminders can ensure that the payment schedule is adhered to without manual follow-up. These reminders can be sent to both parties about upcoming payments or important contract milestones.

Juro's data-rich contract repository and automated reminders can reduce the risks associated with manual tracking and improve visibility into contracts. This is particularly useful for businesses with high contract volumes.

Here are some key features that can help with post-signature management:

- Automated contract reminders

- Centralized repository for all agreements

- Integrations with invoicing systems

These features enable businesses to set up automated invoicing and generate invoices in demand, based on a contract's status in Juro. This can help streamline the payment process and reduce the risk of errors or disputes.

Best Practices and Resources

As a freelancer, you want to make sure you're protected and get paid on time. To do this, ask for upfront payments, such as down payments or full fee upfront invoice payment terms, to ensure you don't get taken advantage of.

You'll also want to make individual terms and conditions for each client, as there's no one-size-fits-all solution. Even within the same industry, clients may have different payment requirements.

To smooth out cash flow for both you and your clients, consider offering Prompt Payment Discounts (PPD). This can be a small discount on your prices, typically 1-3%, for clients who pay quickly.

Here are some payment term options you can consider:

Remember, it's essential to follow industry standards and tailor your payment terms to your business and clients. By doing so, you can avoid complications and ensure a smooth payment process.

Frequently Asked Questions

How do you write terms of payment on an invoice?

To write terms of payment on an invoice, use standard business terms like "Net 30" for 30-day payment, "CIA" for cash in advance, or "20 MFI" for payment by the 20th of the month. Clearly define your payment terms to avoid confusion and ensure timely payments.

Sources

- https://www.billdu.com/blog/understanding-invoice-payment-terms/

- https://www.signwell.com/contracts/payment-agreement-template/

- https://juro.com/contract-templates/payment-agreement

- https://www.invoicesimple.com/blog/how-to-state-invoice-payment-terms-example

- https://www.contractscounsel.com/t/us/payment-terms-agreement

Featured Images: pexels.com