Invoice factoring fees can be a complex and confusing topic, but don't worry, we've got you covered. Factoring fees typically range from 1% to 5% of the invoice amount, depending on the factor and the industry.

The most common fee structure is a markup of 1% to 3% of the invoice amount, plus a flat fee. For example, if you factor an invoice for $10,000 with a 2% markup, you'll pay $200 in fees.

Some factors also charge a flat fee, which can range from $20 to $100 per invoice. This fee is usually a one-time charge, and it's often used in conjunction with a markup.

Discover more: Average Business Loan Amount

What is Invoice Factoring?

Invoice factoring is a financial solution where businesses sell their outstanding invoices to a third-party company, called a factor, to receive immediate payment.

This allows businesses to access cash quickly, often within 24 hours, which can be a lifesaver for cash-strapped companies.

The factor then collects payment from the customer, minus a fee, which can range from 1-5% of the invoice value.

For another approach, see: Company Cash Advance

What Is

Invoice factoring is a financial solution that allows businesses to receive immediate payment for outstanding invoices. Factoring companies provide the funds, typically 80-90% of the invoice value, and handle the collection process.

This process is a win-win for both the business and the factoring company. The business gets the cash they need, and the factoring company gets a percentage of the invoice amount as a fee.

The factoring company will typically hold back 10-20% of the invoice value as a reserve, which is released once the customer pays the invoice in full. This reserve is a safety net for the factoring company, ensuring they don't lose money if the customer doesn't pay.

Invoice factoring can be a game-changer for businesses with slow-paying customers or those experiencing cash flow problems.

Here's an interesting read: No Cash Advance Fee

How It Works

Invoice factoring is a type of financing that's fairly simple and straightforward.

The process begins with a business selling its outstanding invoices to a third-party company, known as a factor. This is a common practice that can help businesses access cash quickly.

Factoring is not a loan, but rather a sale of the invoice to the factor. The factor then collects the payment from the customer, minus a fee.

The factor's fee can vary depending on the industry and the amount of the invoice, but it's typically a percentage of the invoice's value.

Types of Invoice Factoring

Invoice factoring is a financial service that can help businesses manage their cash flow, but there are different types to consider.

There are several types of invoice factoring, including recourse and non-recourse factoring.

Recourse factoring allows the factoring company to pursue the customer for payment if the invoice is not paid, which can be a risk for the business owner.

Non-recourse factoring, on the other hand, transfers all the risk to the factoring company, which means they will cover any losses if the customer doesn't pay.

Another type of factoring is spot factoring, which is used for individual invoices rather than ongoing business.

Cost Components

Invoice factoring fees have two basic parts: the discount fee and the service fee. These fees are usually determined by multiple factors.

The specific rate of these fees depends on several variables, including the size of your borrowing need and the creditworthiness of your customers. Some of these variables are out of your direct control.

The main drivers of factoring rates and fees are the size of your borrowing need, the creditworthiness of your customers, invoice amount and the age of your receivables, and whether all or only select invoices will be financed.

Here are the key variables to consider that influence factoring costs:

- The size of your borrowing need

- The creditworthiness of your customers

- Invoice amount and the age of your receivables

- Whether all or only select invoices will be financed

Invoice factoring fees can vary from company to company, so it's essential to check with your invoice factoring service before getting started.

Fees and Charges

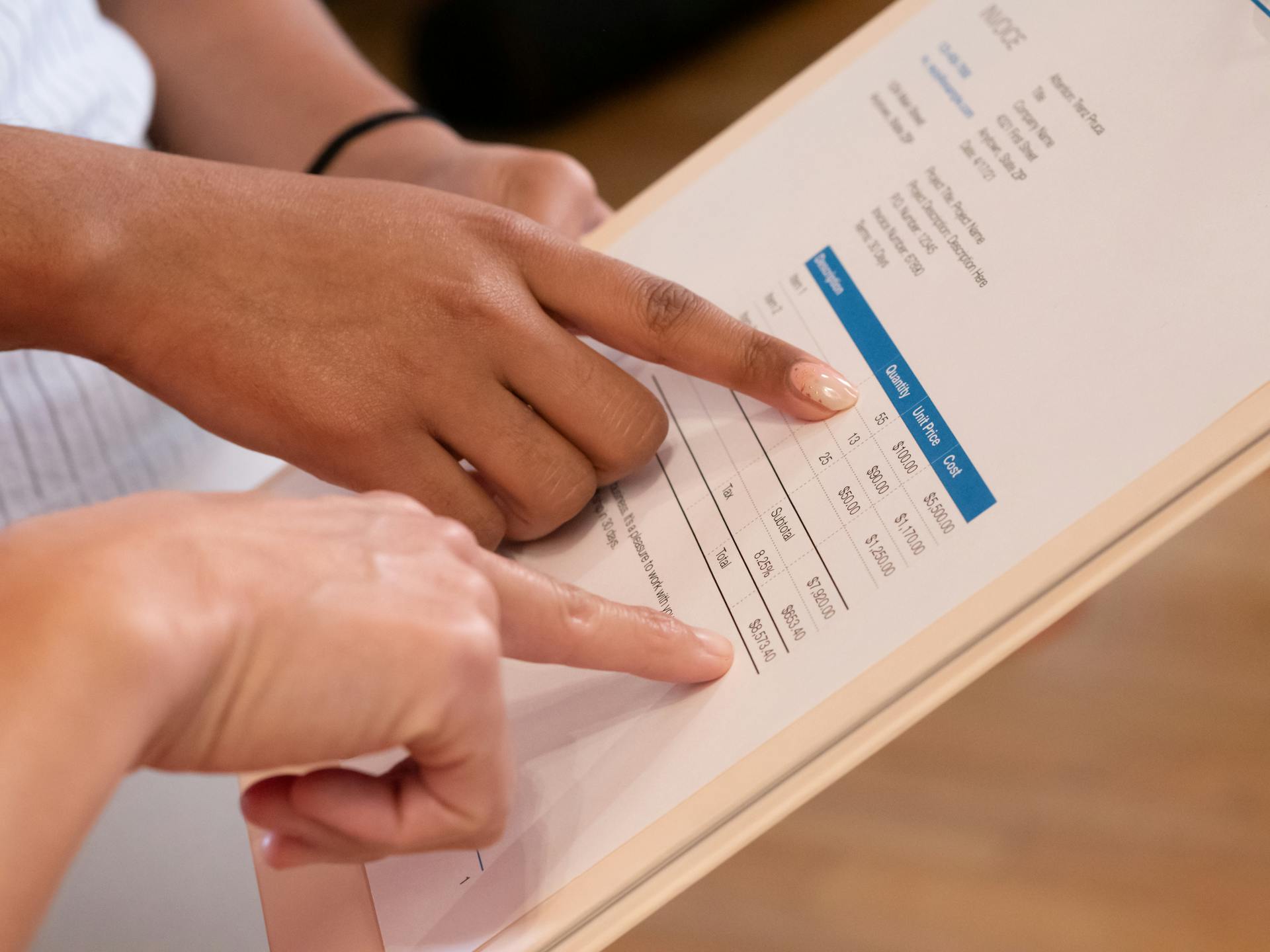

Invoice factoring fees can be broken down into several categories, each with its own specific costs. The discount fee is the most common type of fee, ranging from 1.5% to 5% of the invoice value.

This fee is calculated as an annual rate and charged on a weekly or monthly basis. For example, a 5% discount fee on a $100,000 invoice would result in a charge of $410.95 per year.

The service fee is another type of fee, typically ranging from 0.5% to 2.5% of the invoice value. This fee covers the administration costs associated with processing and managing invoices.

Application fees, on the other hand, can vary widely, ranging from zero to a few thousand dollars. Some companies charge application fees upfront, while others recover the fee by increasing your initial financing fees.

Here are some examples of invoice factoring fees:

It's essential to understand these fees and charges to make an informed decision when choosing an invoice factoring company.

Example

Let's take a closer look at the fees and charges associated with invoice factoring.

A factoring fee of 2% can add up quickly, as we see in the example where a 2% fee on a $100,000 invoice amounts to $2,000.

The initial cash advance is typically a percentage of the invoice face value, and in this example, it's 90% of $100,000, which equals $90,000.

This leaves a remaining advance of $8,000, which is the difference between the invoice face value and the initial cash advance.

The total received from the factoring process is then $98,000, which is the sum of the initial cash advance and the remaining advance.

Here's a breakdown of the numbers:

Non-Recourse

Non-Recourse factoring is a type of factoring where the factoring company assumes the risk of collecting the debt if the buyer fails to pay. This is a lower-risk option for businesses that can't absorb the cost of unpaid invoices.

Non-Recourse factoring costs more than Recourse factoring, but it's a good option for businesses with a better credit rating. Qualifying for Non-Recourse factoring requires a better credit rating.

With Non-Recourse factoring, the factor assumes all the risk of collecting the debt, which is a lower-risk option for small businesses. However, it does cost slightly more than Recourse factoring.

A different take: Debt Factoring

Larger corporations often favor Recourse factoring because they can afford to return the funds they received from selling the uncollectible invoice to the factoring company. If a customer fails to pay, they can return the funds.

Non-Recourse factoring is a good option for businesses that sell to large companies like Walmart or the Federal Government, where the chances of not paying are small. In this case, paying a premium for Non-Recourse starts to look less attractive.

In a Non-Recourse invoice factoring agreement, if your customer pays the invoice in 45 days or less, your total invoice factoring cost with a factoring company like Triumph would average approximately 3.9% of the invoice.

Disclosed

Disclosed factoring is a type of factoring where borrowers' customers are aware of the factoring agreement in place. The customers receive a Notice of Assignment, informing them they are to pay the factoring company moving forward, rather than their vendor (the borrower).

In disclosed factoring, the customers are typically notified in advance, which can help prevent any confusion or disputes. This transparency can also help maintain a good relationship between the borrower and their customers.

The factoring fee, which can range from 2% as seen in the example, is typically disclosed to the borrower and their customers. This fee is usually a percentage of the invoice face value, as shown in the example where a 2% factoring fee on a $100,000 invoice equals $2,000.

The initial cash advance, which can be up to 90% as seen in the example, is also typically disclosed to the borrower and their customers. This means that the borrower will receive up to 90% of the invoice face value as an initial advance, with the remaining balance paid out at a later time.

Here's a breakdown of the potential additional costs that might come with invoice factoring, which can include disclosed factoring fees:

Non-Notification

Non-notification factoring can be a sneaky way for factoring companies to keep debtors in the dark.

With non-notification factoring, the factor doesn't send a Notice of Assignment to the debtor, which means the debtor remains unaware of the factoring agreement.

The factor communicates with the debtor as though it's an extension of the borrowing business, keeping the true nature of the arrangement under wraps.

Non-notification factoring is also known as confidential invoice factoring or undisclosed factoring, which gives you an idea of how secretive it can be.

Discount

The discount fee is a percentage of the invoice value, usually ranging from 1.5 to 5%.

It's calculated as an annual rate, then charged on a weekly or monthly basis, and only applies to the funds advanced.

For example, if the discount rate is 5% on a $100,000 invoice, you'd pay $410.95 in a year, which works out to about $33.41 per month.

The discount fee can vary depending on the invoice factoring company you choose, ranging from 1% to 5% of the invoice value.

Intriguing read: Discount Payment Terms

It covers a period of about 30 to 45 days from the day you sell the invoice to the day the receivable is paid.

The cost of paying for your invoices in advance can be as low as 1.5% or as high as 5% of the invoice value each month.

Recommended read: Same Day Invoice Factoring

Service

A service fee is essentially an administration fee that factoring providers charge for a range of services around processing and managing invoices.

It usually lies in the range from 0.5 – 2.5% of the value of invoices factored.

The precise figure depends on multiple factors.

This fee can add up, so it's essential to understand what you're paying for and how it affects your overall costs.

Other Possible Charges

You might be surprised by the range of additional costs associated with invoice factoring. 4 other possible factoring charges to consider are listed below.

Some factoring companies charge a discount fee, which can vary from 1% to 5% of the total invoice value. This fee covers a period of about 30 to 45 days from the day you sell the invoice to the day the receivable is paid.

Service fees are another common charge, typically ranging from 0.5 to 2.5% of the value of invoices factored.

Application (Flat Rate)

Application fees can range from zero to a few thousand dollars.

The amount and method of paying application fees vary depending on the company you're using.

Some companies charge application fees upfront, while others recover the fee by increasing your initial financing fees.

This intricate nature of application fees makes them highly variable.

You'd better watch out for application fees when choosing an invoice factoring company.

Tax Implications of Factored Receivables

Factored receivables can be a complex issue when it comes to taxes. The IRS considers several factors to determine whether factored receivables are taxable.

Business owners may struggle to identify whether factored receivables are subject to taxes payable to the federal government. The IRS examines the purpose of factoring to prevent firms from transferring income overseas or engaging in tax avoidance or evasion.

Factoring is used to transfer income overseas, which can be a taxable issue. The IRS looks at the purpose of factoring to determine its tax implications.

Explore further: Gofundme Fees and Taxes

Common Myths About

You might think that invoice factoring is only for struggling businesses, but that's not true. Factoring can be a great cash flow solution for businesses of all sizes and stages of growth.

Some people believe that factoring is too expensive to be sustainable, but most businesses that are a good fit for factoring have pricing power, meaning they can incrementally increase their prices to compensate for factoring costs.

It's a common myth that you can't use factoring if you have bad credit, but that's not the case. Invoice factoring is often the best fit for businesses with bad credit, as factoring companies care more about the creditworthiness of your customers than you as a business.

Not all factoring companies are created equal – some will try to take advantage of you with hidden fees, float, and other added costs. On the other hand, factors like altLINE are regulated banks that are 100% transparent in their pricing.

See what others are reading: Invoice Factoring for Staffing Companies

Factors Affecting Fees

The size of each invoice and their volume significantly influence your factoring fee. If you're able to guarantee a high volume of invoices, a factoring company will likely offer lower factoring fees.

The discount fee, which ranges from 1.5-5% of the invoice value, only applies to the funds advanced. It's calculated as an annual rate and charged on a weekly or monthly basis.

Invoice frequency also plays a role in factoring fees. It's cheaper to process one large invoice than multiple smaller ones. For example, processing one $20,000 invoice costs less than processing two $10,000 invoices.

Here's a breakdown of the main factors affecting factoring fees:

If your business has previously agreed to a longer payment period, factoring charges will often be higher. The factoring company may simply charge the same discount charge over this period.

Spot

Spot factoring allows you to factor only one invoice, which can be a lifesaver if you have a large outstanding invoice that needs to be paid right away.

Spot factoring is particularly useful for businesses with one-time or irregular sales, such as event planners or seasonal retailers.

This type of factoring is also known as single invoice factoring, and it's a great option for companies that don't need ongoing financing.

By factoring just one invoice, you can get the cash you need without committing to a larger financing arrangement.

How Rates Are Calculated

Calculating factoring rates is a bit more complex than just slapping on a flat fee. The main drivers of factoring rates are the size of your borrowing need, the creditworthiness of your customers, invoice amount, and the age of your receivables.

The size of your invoices and their volume will significantly influence your factoring fee. If you can guarantee a high volume of invoices, a factoring company will likely offer lower factoring fees. Conversely, it's in your interest to have your invoices factored less frequently because this reduces the cost of factoring.

You might like: Invoice Factoring Rates

The creditworthiness of your customers also plays a crucial role in determining factoring rates. A factoring provider will look at your key finance figures, such as turnover and profitability, to calculate what rates to offer.

Factoring fees typically compound for the life of the invoice, though flat-fee structures are available for certain industries like trucking. Typically, fees for factoring services start at around 2%, with a typical advance rate of 80%-90% depending on the industry.

Here's a breakdown of the key factors that affect factoring rates:

- Yearly sales volume

- Creditworthiness of customers

- Typical length of time it takes for customers to pay

- Average size of the invoice

These factors will be highlighted in your factoring contract, which is essential to read and understand.

Industry

Industry plays a significant role in determining the cost of factoring, with certain sectors being considered higher risk than others.

Retail, agriculture, and even accounting are seen as relatively high-risk industries. This is reflected in the cost of factoring, which can be higher for businesses in these sectors.

Gambling and alcohol industries are even more high-risk, with a corresponding increase in factoring costs.

On the other hand, industries like scientific research, laboratory wholesalers, and flying schools are considered low-risk, resulting in lower factoring costs.

Factoring companies that specialize in a particular industry can help reduce the risk factor and lower costs for businesses in that sector.

Frequently Asked Questions

Is invoice factoring worth it?

Consider invoice factoring if you need immediate cash to cover operational costs or invest in growth, but weigh the benefits against potential fees and terms

What is the interest rate for invoice financing?

Invoice financing interest rates typically range from 7% to 12% per annum, or between 1% to 3% per month with some non-bank lenders. Understanding the interest rate is crucial to making informed decisions about invoice financing.

Sources

- https://www.trevipay.com/resource-center/blog/how-much-does-invoice-factoring-cost/

- https://www.factorfinders.com/factoring-fees/

- https://www.crownfactoringservices.com/blog/invoice-factoring-cost-overview

- https://altline.sobanco.com/invoice-factoring/

- https://www.invoicefactoring.com/what-is-invoice-factoring/

Featured Images: pexels.com