Banking and payments can be confusing, especially with the rise of digital transactions. Cheques are still widely accepted and used for various purposes.

A cheque can be used to pay bills, settle debts, or even make purchases from certain retailers. It's a secure way to make payments, especially for large amounts.

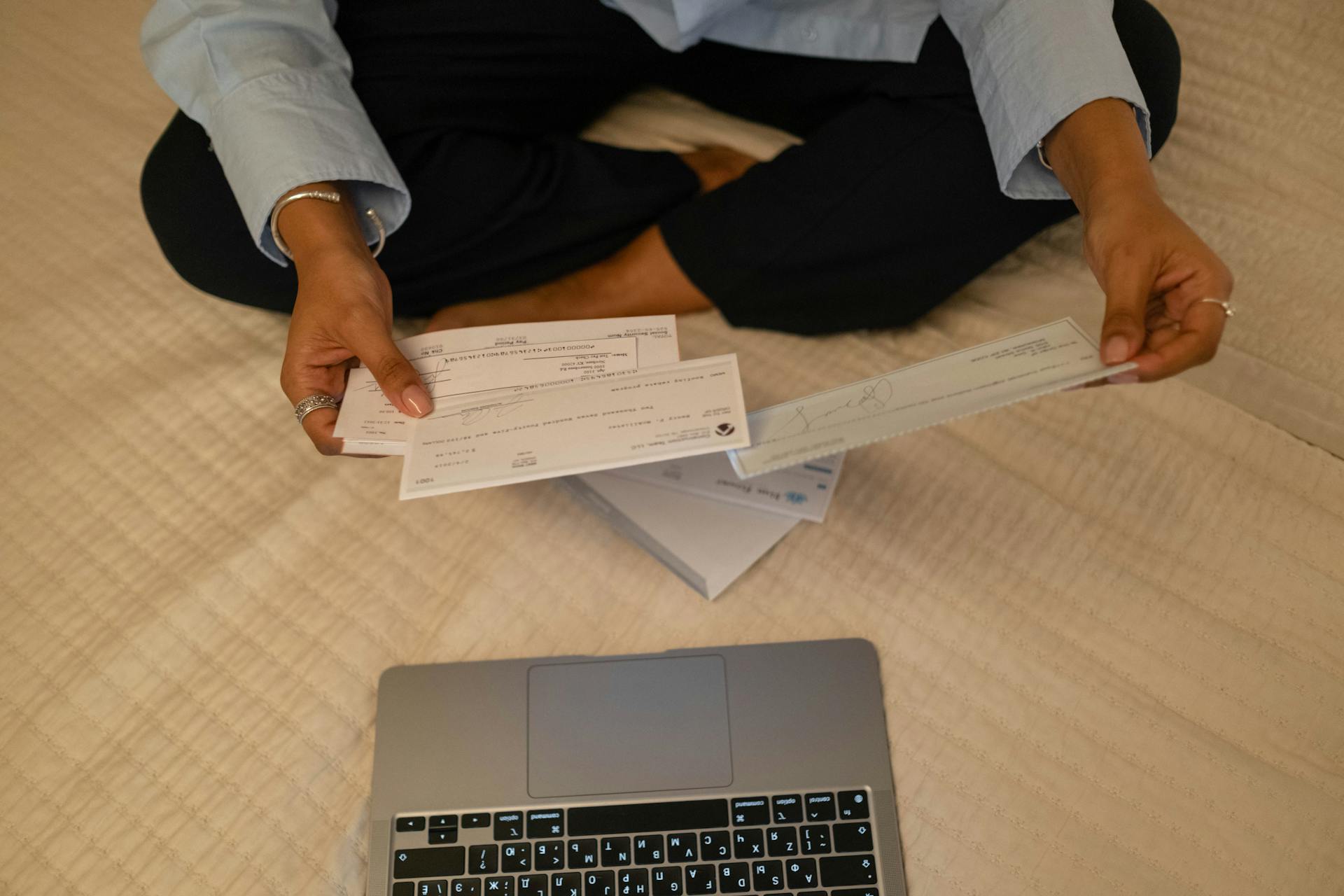

To write a cheque, you'll need to fill in the payee's name, the amount in words and numbers, and the date. The payee's name should be written in full, without any abbreviations.

Cheques can take a few days to clear, so it's essential to plan ahead and give the recipient enough time to deposit the cheque. This can vary depending on the bank and the type of cheque.

Here's an interesting read: Quickbooks Online Payments Bank to Bank

What is a Check?

A check is a written, dated, and signed draft that directs a bank to pay a specific sum of money to the bearer.

The person writing the check is called the payor or drawer, while the person to whom the check is written is the payee.

The bank on which the check is drawn is called the drawee.

A check is a common way to transfer funds, and it's often used for everyday transactions.

How Checks Work

A check is a bill of exchange or document that guarantees a certain amount of money. It's printed for the drawing bank to provide to an account holder (the payor) to use.

The payor writes the check and gives it to the payee, who then takes it to their bank for cash or to deposit into an account. This is a more secure way of transferring money than cash, especially with large sums.

Checks essentially provide a way to instruct the bank to transfer funds from the payor’s account to the payee or the payee’s account. This is done without using physical currency.

Here are the key lines that need to be filled in by the payor:

- Date

- Payer's name and bank information

- Payee's name

- Amount of the check in a dollar figure

- Amount written out in words

- Payer's signature

Process

So you want to know how to process a check? Well, first things first, the payor writes the check and gives it to the payee, who then takes it to their bank for cash or to deposit into an account.

The check essentially provides a way to instruct the bank to transfer funds from the payor's account to the payee's account. This is a substitute for physical currency, making it a more secure way to transfer money, especially with large sums.

The payor needs to fill in several lines on the check, but we'll get to that later. For now, let's focus on the process.

Here are the steps to follow when processing a check:

And that's it! By following these steps, you'll be able to process a check with ease.

Cashing and Validating Payments

Cashing a cheque is a straightforward process, but it's essential to know the options and requirements. You can cash a cheque at a bank, an ATM, or on your bank's website or app. Take the cheque, a photo I.D., and bank card or account number to a teller.

If you're an account holder with the bank, many banks will cash cheques without charging a fee. However, some banks may require you to deposit the cheque to your account rather than cash it, especially if the cheque is from an account at another bank. You'll need to take the cheque, a photo ID, and your account number to any teller.

Expand your knowledge: Federal Reserve Bank Services Check Routing Number

If you don't have an account, you can visit the bank that issued the cheque. Take the endorsed cheque and your photo I.D. to a teller window. Give the cheque and your I.D. to the teller and explain that you don’t have an account, but the cheque is from an account holder at their bank.

To cash a cheque, you'll need a valid photo I.D. Driver’s licenses and passports are usually the best choices. In some cases, military or school I.D.s may be accepted. You can also cash a cheque at a retail store, such as a grocery or big-box store, or use a prepaid card to load the funds onto a card.

Before cashing a cheque, it's crucial to verify its validity. Make sure the cheque is made out to you, with your name written correctly. Also, ensure all the information on the cheque is complete and accurate, including the date, amount of payment, and signature. If the information is invalid or missing, your bank will refuse payment on the cheque.

Here's a quick checklist to help you verify a cheque's validity:

- Verify the trustworthiness of the person writing the cheque.

- Make sure the cheque is made out to you.

- Verify all the info on the cheque, including the date, amount of payment, and signature.

- Endorse the cheque when you're ready to cash it.

Types of Checks

A certified check is a type of check that verifies the drawer's account has enough funds to honor the amount, guaranteeing it won't bounce.

There are several types of checks, including certified checks, cashier's checks, and payroll checks, each used for different purposes.

A certified check must be presented at the bank from which it is drawn to ensure its authenticity with the payor.

Certified checks are useful for large transactions or when you need to guarantee payment.

Take a look at this: Can You Get a Certified Check at Any Bank

Check Features and Risks

A check is a written, dated, and signed draft that directs a bank to pay a specific sum of money to the bearer.

The payor must fill in several lines when writing a check, including the date, the payee line, the amount of the check, the payor's endorsement, and a memo line. This information is crucial for the bank to process the transaction.

If a check is lost or stolen, a third party is not able to cash it, as the payee is the only one who can negotiate the check, making it a more secure way of transferring money than cash.

For your interest: Checking Account with Overdraft Line of Credit

Here are the key features of a check:

- Date: The date the check is written.

- Payer line: The name of the person or business writing the check.

- Payee line: The name of the person or business receiving the check.

- Amount of the check: The amount of money being transferred.

- Payor's endorsement: The payor's signature, verifying the transaction.

- Memo line: A line for the payor to add a note or description of the transaction.

Key Features

A certified check verifies that the drawer's account has enough funds to honor the amount of the check. This type of check is guaranteed not to bounce.

A check typically features the date, payee line, amount, payor's endorsement, and a memo line.

In some countries, such as Canada and England, the spelling used is "cheque".

Dishonoured Checks

A dishonoured cheque is essentially a cheque that's been refused by the payer's bank, and it's often referred to as a bounced cheque. This can happen for various reasons, including insufficient funds in the drawer's account.

A bounced cheque can't be redeemed for its value and is essentially worthless. It's also known as an NSF (non-sufficient funds) cheque or a returned deposit item. Banks typically charge customers for issuing a dishonoured cheque.

In some cases, a cheque may be dishonoured because the drawer's account has been frozen or limited. This can be a serious issue, and it's essential to take care of your finances to avoid such situations.

Issuing a stop on a cheque is another way to prevent it from being honoured. This instruction tells the financial institution not to honour a particular cheque.

Expand your knowledge: Acquiring Bank vs Issuing Bank

Banking and Checks

Checks are a common way to transfer funds between two parties, and they're generally seen as a more secure way of transferring money than cash, especially with large sums. If a check is lost or stolen, a third party is not able to cash it, as the payee is the only one who can negotiate the check.

There are several types of checks, including certified checks, which verify that the drawer's account has enough funds to honor the amount of the check. Certified checks are guaranteed not to bounce.

To deposit a check, you can go to your bank and follow a few simple steps: fill out a deposit slip with the required information, attach the check to the slip, and submit them to the bank representative responsible for cheque deposits. Collect the cheque deposit receipt, which is the second perforated section of the deposit slip, stamped by the bank.

Here's a quick rundown of the information you'll need to fill out on the deposit slip:

Banks have different policies on bounced checks, and some may charge overdraft fees or non-sufficient funds fees. Some banks may even provide a grace period, such as 24 hours, in which time you can deposit funds to avoid the overdraft fees.

Worth a look: Navy Fed Overdraft Protection

Cashier's Check

A cashier's check is a type of check that's considered more secure than a personal check.

It's signed by a bank and drawn against the bank's account, which makes it a guaranteed payment.

Typically, funds from a deposited cashier's check must be available the next business day, but a bank may place a hold on some of those funds if the check exceeds $5,252.

If a bank has reason to believe the check won't clear, it can place a hold on the entire amount.

Expand your knowledge: Capital One Availability of Funds

Payroll Check

A payroll cheque is a type of cheque used to pay wages. It's still commonly referred to as a pay cheque, even though cheques for paying wages are less common today.

See what others are reading: How Does Chase Pay in 4 Work

Payroll cheques issued by the military or government entities to their employees are referred to as warrants. This is a specific type of payroll cheque.

To deposit a payroll cheque, you'll need to follow the same steps as depositing a regular cheque. This includes obtaining a cheque deposit slip and filling it out with the required information.

The required information on the deposit slip includes the name as it appears on the cheque, bank account number, the amount mentioned on the cheque, and the name and branch of the bank where the cheque is drawn. You'll need to fill this information twice, on separate perforated sections of the slip.

Double-checking the details on the deposit slip is crucial to ensure accuracy. Errors can prevent funds from being deposited into your account.

Here's a summary of the information you'll need to fill out on the deposit slip:

Attach the cheque to the deposit slip and submit them to the bank representative responsible for cheque deposits. Collect the cheque deposit receipt, which is the second perforated section of the deposit slip, stamped by the bank.

Bounced Checks

Bounced checks can be a real hassle, and it's essential to understand what happens when you write a check with insufficient funds.

A bounced check occurs when the account holder writes a check for an amount larger than what is held in their checking account.

This is because there are insufficient or non-sufficient funds (NSF) in the account, and the check cannot be processed.

A bounced check usually results in a penalty fee for the payor, which can range from $20 to $35 or more.

The payee may also be charged a fee in some cases, adding to the overall cost of the bounced check.

Returned deposit item fees are another type of charge that can occur when depositing a bounced check into your account.

Waiving Fees

Some banks offer fee waivers for customers who maintain a minimum balance in their account. For instance, if you keep $1,000 or more in your checking account, you might be exempt from overdraft fees.

Banks also waive fees for first-time overdrafts, allowing you to recover from a mistake without incurring a penalty. This can be a lifesaver if you're short on cash and need to cover an unexpected expense.

If you're unable to pay a fee, some banks allow you to dispute it and have it waived. This is typically done through the bank's customer service department.

Depositing Electronically

You can deposit a cheque electronically using your bank's app. Many banks now allow this method, making it convenient to deposit cheques remotely.

To start, you'll need to download your bank's mobile banking app from your phone's app store and connect it to your account. Follow the app's directions and enter your name and account details to set it up.

Once you have the app set up, log in and select "deposit" to begin the process. If you're new to mobile banking, don't worry, it's easy to navigate.

Intriguing read: Td Bank Mobile Banking App

Take photos of the front and back of your cheque using the app. Make sure to sign the back of the cheque before taking a photo. The app will guide you through the process to get a clear image.

Enter the amount on the cheque and confirm it's correct. The app will prompt you to do this after you've taken the photos.

History and Variations

Checks have been around since ancient times, with some believing a type of check was used among the ancient Romans.

The modern check, however, became popular in the 20th century. Check usage surged in the 1950s as the check process became automated and machines were able to sort and clear checks.

The oldest surviving American checkbook dates to the 1790s, from the Bank of New York.

History of Checks

Checks have been around for a long time, with some people believing they were used by the ancient Romans.

The modern checks we use today became popular in the 20th century, especially in the 1950s when automation made the check process faster and more efficient.

Check cards, which were first created in the 1960s, were essentially the precursors to today's debit cards.

Credit and debit cards have since become the dominant means of payment, making checks somewhat less common.

The oldest surviving American checkbook dates back to the 1790s, specifically from the Bank of New York.

A unique perspective: Umpqua Secured Credit Card

Variations on Regular Checks

Regular cheques have undergone significant changes over time to address specific needs or issues.

One variation is the pre-printed cheque form, pioneered by the Bank of England in 1717, to prevent fraud. This innovation required customers to attend the bank in person to obtain a numbered form.

The use of cheque paper to prevent fraud highlights the importance of security measures in cheque writing.

In some countries, such as the US, the payee can endorse the cheque, allowing them to specify a third party to whom it should be paid.

See what others are reading: List of Banks That Have Merged to Form the State Bank of India

Around the World

As we explore the world of history and variations, let's take a look at how different cultures have shaped the way we live today.

In Japan, the traditional tea ceremony has been a cornerstone of the country's culture for centuries, with the first recorded ceremony dating back to the 9th century.

From Japan to India, the art of yoga has been practiced for over 5,000 years, originating in the Indus Valley Civilization.

In the Middle East, the ancient city of Petra was carved into the sandstone cliffs over 2,000 years ago, serving as the capital of the Nabataean Kingdom.

The ancient Greeks were known for their love of philosophy, with famous philosophers like Socrates, Plato, and Aristotle shaping the way we think about the world today.

In Africa, the Maasai people have been living in harmony with the land for centuries, with their traditional lifestyle centered around herding and farming.

The ancient Egyptians were master builders, constructing some of the most impressive pyramids in history, including the Great Pyramid of Giza, which took over 20 years to build.

Tips and Consumer Reporting

Consider depositing a cheque you receive rather than cashing it. Your bank will place the funds in your account and then collect the funds from the bank from which the cheque is drawn. This may cause a delay of a few days.

If you're planning to cash a cheque, do it within 6 months of its written date. After that, banks are not obligated to honor it.

Some cheques may be made out to "_____ or bearer", which means anyone with physical possession of the cheque can cash it.

Tips

If you receive a cheque, consider depositing it rather than cashing it, as your bank will ensure the funds are collected from the issuing bank.

You may have to wait a few days to spend the money, as the bank will verify the cheque is honored by the other bank.

Banks are not obligated to honor cheques older than 6 months, so make sure to cash your cheque within this timeframe.

Some cheques may be made out to "_____ or bearer", which means anyone with physical possession of the cheque can cash it.

Here are some key cheque-related tips to keep in mind:

Consumer Reporting

In the United States, consumer reporting agencies track how people manage their chequing accounts, providing cheque verification services that screen chequing account applicants.

Banks use these agencies to screen applicants and deny those with low debit scores due to the risk of overdrawn accounts.

In the UK, dishonoured cheques can be reported on a customer's credit file, just like Direct Debits or standing orders, but not individually and not universally amongst all banks.

Dishonoured payments from current accounts can be marked as missed payments on the customer's credit report.

Check this out: Toronto Dominion Bank Accounts

Frequently Asked Questions

What is the bank on a cheque?

The bank on a cheque is identified by a three-digit institution number at the bottom of the cheque. This number represents the bank where your account was opened.

Sources

- https://www.investopedia.com/terms/c/check.asp

- https://www.hdfcbank.com/personal/resources/learning-centre/save/different-types-of-cheque-you-need-to-know

- https://en.wikipedia.org/wiki/Cheque

- https://www.wikihow.com/Cash-a-Cheque

- https://www.dbs.com/digibank/in/articles/save/how-to-deposit-cheque-in-bank

Featured Images: pexels.com